How Bakkt Could Reveal the Natural Demand in Bitcoin Market

Like any commodity or asset, bitcoin's price tells the story of supply and demand. Exchange volume is largely a gauge of speculation and true on-chain transaction health is obfuscated by mixers, tumblers and anomalies and a meaningful metric for "economic activity" or natural demand is still to be found.

with no reliance on cash platforms for settlement prices a one-day physically settled bitcoin contract will serve as a price discovery contract Bakkt mission statement

Natural demand for a physical asset is needed to sustain the price of any commodity long-term outside of paper derivatives like swaps, forwards, futures or even an ETF. For instance, in the oil market, Chinese import numbers have been growing steadily for years (China is the largest importer of oil) but because it is hoarding vast stocks of oil and not using it, any increase in Chinese inventories now has a negative impact on oil prices as it isn't interpreted as natural demand.

In some commodity markets, like oil, inventory numbers are watched for build-ups and drawdowns in certain regions, like the Cushing hub in the US, and similar hubs in Saudi Arabia and Dubai. Inventory build-ups are negative as it shows a lack of natural demand in the market with drawdowns largely positive for price.

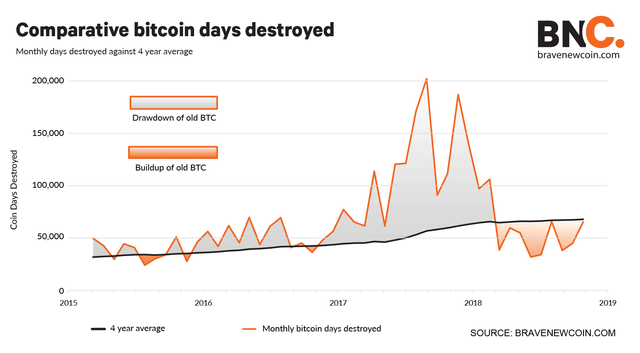

_The Bitcoin Days Destroyed metric is negative when it is above its 4 year average (black line). Bakkt proposes to create more long-term (old BTC) holders with its deliverable futures contract. _

In a similar manner to inventory counts in oil we can use the 'Bitcoin Days Destroyed' metric to gauge build-up and drawdown in old bitcoins held in cold storage. In this case, the higher the days destroyed count the higher the drawdown of old BTC and the more it's being used for speculation rather than its intended use - either as a store of value or as a unit of exchange - so drawdowns are negative for price and build-ups are positive.

Bakkt proposes to create a market for long-term holders such as hedge funds and wealth managers like Fidelity that wish to hold the underlying asset in cold storage as opposed to speculate on price with bitcoin futures from Cboe and CME.

How deliverable futures are settled

Although there are futures markets in most assets, not all are cash settled - most require physical delivery. It is the manufacturers and producers of a raw commodity such as coffee, oil, grains, gold etc, which are the typical hedgers in deliverable futures markets. The buyer of a deliverable futures contract buys it in the denominated currency and will take delivery of the underlying asset when the contract expires, while the person who sells or sells short the contract must deliver the physical asset.

The CME gold futures contract (GC) is also a deliverable contract that must be settled with delivery of the underlying asset. If a manufacturer knows that they need to buy gold in six months when the spot price is $1,200/ounce and the futures price is $1,100/ounce they will buy the futures contract to lock in the price to buy it at a discount in six months time. Conversely, if the manufacturer knows they will be selling in six months when the spot is $1,200/ounce and the futures is $1,100, then they will short the futures contract to guarantee they can sell at $1,100 in case the spot price is lower than that in six months.

In the 1930s, economist John Maynard Keynes described commodities futures prices as the net position of hedgers or the transfer of risk from hedgers to speculators.

The importance of physical versus paper ratio

Bitcoin exponents, such as Andreas Antonopoulos, have forewarned of bitcoin derivatives and ETFs bringing duplication and manipulation of the amount of "bitcoin" in the market which dilutes the price of the underlying asset and increases speculative demand over real demand, something that has been happening for years in the traditional commodity markets.

Gold and silver are often cited as markets with an imbalance of paper derivatives to physical assets. The ratio of paper versus physical gold has accelerated since the proliferation of gold funds and ETFs, with the circulation of paper-backed gold now outnumbering physical gold per ounce at the Chicago Mercantile Exchange's Commodity Exchange (COMEX) by 360:1. Stated differently, the gold market is nearly 300% artificial.

Short selling of futures and various "paper" gold has been attributed to suppressing the spot price of gold and creating a ceiling at around $1,800 per ounce and there is no reason why the proliferation of derivatives wouldn't create a similar ceiling in the price of bitcoin.

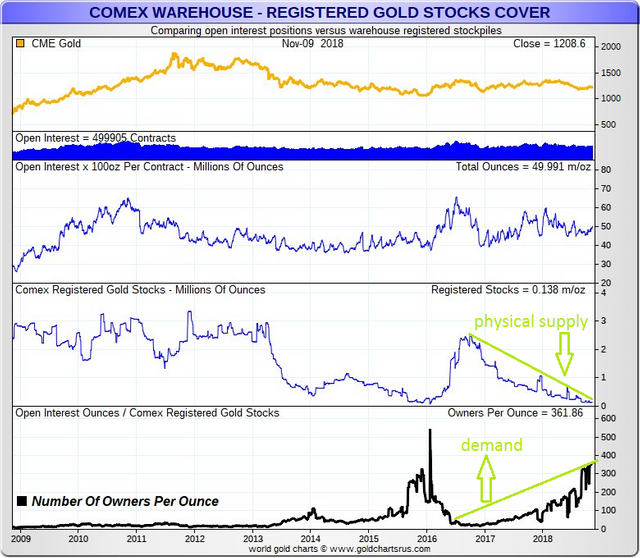

The Chicago Mercantile Exchange's COMEX is one of the largest metals futures markets in the world (though much smaller than the London Metal Exchange) and the ratio of open interest to registered gold stocks (the bottom panel in black writing) is a barometer for supply/demand - supply being the physical/deliverable (registered) gold stocks in the Comex vaults and demand the open interest in the futures contracts.

The number of holders of gold futures contracts per ounce of gold at the COMEX warehouse has been rising while the stock of gold per ounce at the warehouse has fallen sharply.

Registered gold stocks (second panel from bottom) shows that the physical, deliverable stockpiles of gold are at record lows. From these levels we can deduce that the price of gold needs to go higher to bring waning supply (physical stores) and soaring demand (open interest) levels back to equilibrium.

As there is a finite/fixed supply rate of gold in the world, price is the only mechanism by which the supply/demand equation can be rebalanced. A very similar supply dynamic is at play in bitcoin.

The stock to flow ratio of gold and bitcoin

The supply situation of gold and bitcoin is similar as all gold that has been mined is still above ground and in circulation (in the form of bars, jewellery or scrap) and, like bitcoin, is only taken out of the market if lost. Like bitcoin, the mining supply has slowed over the years and has become harder and riskier to find as surface level stocks have been depleted.

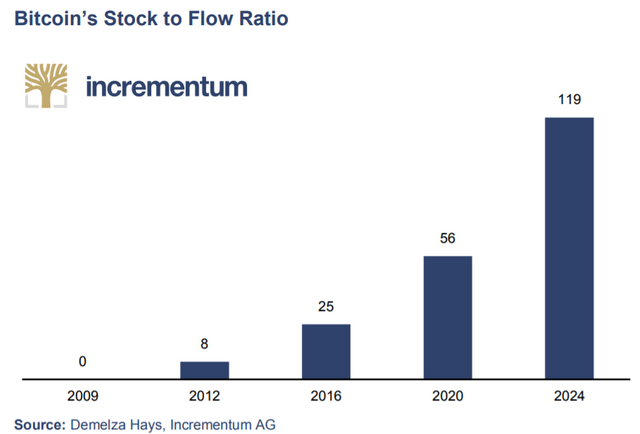

By 2020 the inflation rate of bitcoin will halve from 3.85% currently to 1.8% as the mining reward is halved from 12.5BTC per block to 6.25BTC.

The stock-to-flow (STFr) ratio in gold is the ratio of above ground stocks to annual mine production, measured in years. The supply/flow of gold is quite constant and although not programmed like bitcoin it is predictable, which gives it the deflationary value proposition that attracts investors to both assets as a store of value. Gold's stock-to-flow ratio is around 66 years, whereas bitcoin's is approximately 25 years.

But due to the halving of annual production (in miner's rewards) every four years, the supply will be reduced in 2020 to 6.25BTC per block and thus increase the ratio of the stock-to-flow to 56 years.

Reporting of hedger and speculator positions

In traditional futures markets a weekly positional report is published called the commitment of traders report - analogous to an exchange order book for futures - that shows the open interest in the market and the positions of hedgers versus speculators.

Hedgers are referred to as "commercials", or the producers and manufacturers of the commodity who deal in the physical underlying asset; the "non-commercial" or "large speculators" are investment banks and "small speculators" are the hedge funds. Traders are most concerned with the position of non-commercials as they follow price trend, whereas hedgers take the opposite side to the trend.

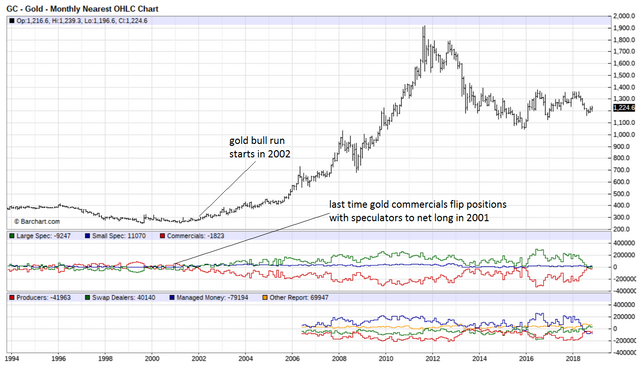

The COT report shows large speculators in the gold futures market (GC) is net long after recently flipping with commercials, those hedging their costs. The crosshair is where momentum flipped.

Commercials (producers) of commodities take short positions to cover (hedge against) falling prices to sell at a certain price in the future in case it goes lower. As we can see from the above gold chart, the positions of speculators flipped from short to long around the same time that price started a bullish trend reversal.

The last time gold commercials flipped positions to net long to hedge against falling prices was in 2001 and was followed a year later by an eight-year bull run.

The recent positional flip of speculators - commercials turning net positive and speculators net short - is the first since early 2001, just before the bull run in gold took place.

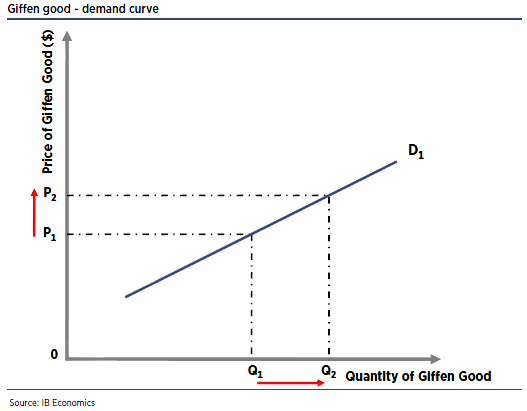

Gold and bitcoin as a giffen good

Regardless of 'Satoshi's Vision' bitcoin's only foreseeable use is as digital gold. Price appreciation is the only reason people want it, as evidenced by the prioritizing of building trading infrastructure and cold storage over merchant adoption.

So far demand for bitcoin has only risen along with its price, despite there being no shortage of supply. Like gold it exhibits some of the same conditions that can be described as a 'Giffen good'. A Giffen good is an asset/product whose price defies the conventional dynamics of price and demand - as its price goes up so to does demand for the product.

Examples normally given are low quality staple foods - as the price rises, people can't afford to buy better quality foods and are forced to purchase more of the staple - but there are many assets that observe the same behaviour, including gold and bitcoin de facto of digital gold.

Some economists argue that there are three necessary pre-conditions for a Giffen good:

Conclusion

As stated in its mission, Bakkt is likely to create more market transparency and better price discovery. Hedge funds and wealth managers will be the most likely first users, though Bakkt could also take some market share from the opaque OTC markets which are presumed to be an even larger marketplace than exchanges for large institutions and miners to trade "physical" bitcoin.

Bakkt could also help to identify the positions of net hedgers and speculators in the futures markets like the commitment of traders for regular commodities, although this would require a lot of participation in the market and presuming it becomes the primary traded contract among hedgers and speculators.

Details are still relatively scant and it is yet to be revealed which spot benchmark price Bakkt will base its futures contracts on (the CME's XBT contract for instance is priced on Gemini's bitcoin spot).

In the medium term bitcoin's best hope for an uplift in price is to mimic gold in its traits as a Giffen good with demand moving in tandem with price to supplement people's incomes as they erode with inflation or recession. If Bakkt's market does indeed prove successful it only reinforces bitcoin's role as a store of value rather than a medium of exchange - a decoupling that would be positive for long-term price.