Fundings & Exits – TechCrunch

Workday acquires Rallyteam to fuel machine learning efforts

Sometimes you acquire a company for the assets and sometimes you do it for the talent. Today Workday announced it was buying Rallyteam, a San Francisco startup that helps companies keep talented employees by matching them with more challenging opportunities in-house.

The companies did not share the purchase price or the number of Rallyteam employees who would be joining Workday .

In this case, Workday appears to be acquiring the talent. It wants to take the Rallyteam team and incorporate it into the company’s engineering unit to beef up its machine learning efforts, while taking advantage of the expertise it has built up over the years connecting employees with interesting internal projects.

“With Rallyteam, we gain incredible team members who created a talent mobility platform that uses machine learning to help companies better understand and optimize their workforces by matching a worker’s interests, skills and connections with relevant jobs, projects, tasks and people,” Workday’s Cristina Goldt wrote in a blog post announcing the acquisition.

Rallyteam, which was founded in 2013, and launched at TechCrunch Disrupt San Francisco in September 2014, helps employees find interesting internal projects that might otherwise get outsourced. “I knew there were opportunities that existed [internally] because as a manager, I was constantly outsourcing projects even though I knew there had to be people in the company that could solve this problem,” Rallyteam’s Huan Ho told TechCrunch’s Frederic Lardinois at the launch. Rallyteam was a service designed to solve this issue.

[gallery ids="1055100,1053586,1053580,1053581"]Last fall the company raised $8.6 million led by Norwest Ventures with participation from Storm Ventures, Cornerstone OnDemand and Wilson Sonsini.

Workday provides a SaaS platform for human resources and finance, so the Rallyteam approach fits nicely within the scope of the Workday business. This is the 10th acquisition for Workday and the second this year.

Chart: Crunchbase

Workday raised over $230 million before going public in 2012.

Alibaba’s Ant Financial fintech affiliate raises $14 billion to continue its global expansion

Ant Financial, the financial services affiliate connected to Alibaba which operates the Alipay mobile payment service, has confirmed that it has closed a Series C funding round that totals an enormous $14 billion.

The rumors have been flying about this huge financing deal for the past month or so, with multiple publications reporting that Ant — which has been strongly linked with an IPO — was in the market to raise at least $9 billion at a valuation of upwards of $100 billion. That turned out to be just the tip of the iceberg here.

The money comes via a tranche of U.S. dollar financing and Chinese RMB from local investors. Those names include Singapore-based sovereign funds GIC and Temasek, Malaysian sovereign fund Khazanah Nasional Berhad, Warburg Pincus, Canada Pension Plan Investment Board, Silver Lake and General Atlantic.

Ant said that the money will go towards extending its global expansion (and deepening its presence in non-China markets it has already entered), developing technology and hiring.

“We are pleased to welcome these investors as partners, who share our vision and mission, to embark on our journey to further promote inclusive finance globally and bring equal opportunities to the world. We are proud of, and inspired by, the transformation we have affected in the lives of ordinary people and small businesses over the past 14 years,” Ant Financial CEO and executive chairman Eric Jing said in a statement.

Alibaba itself doesn’t invest in Ant, which it span off shortly before its mega-IPO in the U.S. in 2014, but the company did recently take up an option to own 33 percent of Ant’s shares.

Ant has long been tipped to go public. Back in 2016 when it raised a then blockbuster $4.5 billion — little did we know it would pull in many multiples more — the company has been reportedly considering a public listing, but it instead opted to raise new capital at a valuation of $60 billion.

It looks like the same again, but with higher stakes. This new Series C round pushes that valuation up to $100 billion, according to Bloomberg. (Ant didn’t comment on its valuation.) So what has Ant done over the past two years to justify that jump?

It has long been a key fintech company in China, where it claims to serve offer 500 million consumers and offers Alipay, digital banking and investment services, but it has begun to replicate that business overseas in recent years. In particular, it has made investments and set up joint-ventures and new businesses in a slew of Asian countries that include India, Thailand, Korea, Indonesia, Hong Kong, Malaysia, the Philippines, Pakistan and Bangladesh.

The company was, however, unsuccessful in its effort to buy MoneyGram after the U.S. government blocked the $1.2 billion deal.

On the business-side, Ant is said to have posted a $1.4 billion profit over the last year, suggesting it is more than ready to make the leap to being a public firm.

Despite that U.S. deal setback, Ant said today that its global footprint extends to 870 million consumers. I’d take that with a pinch of salt at this point since its business outside of China is in its early stages, but there seems little doubt that it is on the road to replicating its scale in its homeland in many parts of Asia. Raising this huge round only solidifies those plans by providing the kind of capital infusion that tops most of the world’s IPOs in one fell swoop.

Rakuten acquires mobile commerce startup Curbside

Tokyo-headquartered Rakuten, Japan’s answer to Amazon, is acquiring the Silicon Valley mobile ordering and pickup startup Curbside, the companies announced today. Terms of the all-cash deal were not disclosed, but Curbside had previously raised between $40 million and $50 million from investors including CVS, Index Ventures, Sutter Hull Ventures, AME Cloud Ventures, Qualcomm Ventures, Chicago Ventures, and others.

Founded in 2013 by former Apple engineers with backgrounds in location-based technology, Curbside was one of the early startups to capitalize on the idea that e-commerce’s expansion won’t entirely involve ship-to-home deliveries, but could also include the convenience of online ordering with a curbside pickup option at bricks-and-mortar retailers to speed things up.

The company first launched its own mobile shopping app with a limited set of partners, including a shopping center in San Jose and a handful of San Francisco Bay area Target stores. The Target test wrapped up some time ago, and Target instead launched its own Drive Up curbside pickup this year – possibly encouraged by the potential it saw through its tests with the third party.

Curbside then went on to power mobile orders and store pickup for CVS, which invested in the company as a strategic partner back in 2016.

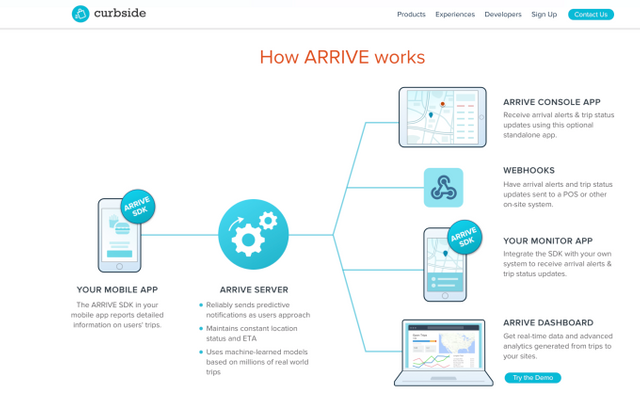

The startup also developed an SDK for mobile app developers called ARRIVE that allows retailers to see when customers are arriving at their location for things like order pickup, mobile order ahead, and appointment checkin. CVS, Sephora, Chipotle, Nordstrom, Pizza Hut, Chevron, Boston Market, Westfield, HEB, and Yelp are listed on the Curbside website as ARRIVE customers.

For strategic partner CVS in particular, Curbside is available at thousands of locations across the U.S. for order ahead and pickup.

ARRIVE has since become the primary business for Curbside, and now contributes to the majority of its revenue. Curbside CEO Jaron Waldman says half of the top ten QSR’s (quick serve restaurants) are now using ARRIVE, as the restaurant side of the ARRIVE business has really taken off. These operations will continue as planned, Curbside says.

Across its customer base, Curbside has powered several million curbside pickups to date, and has over 8,000 U.S. locations, as well as some traction in non-U.S. markets, including Canada and India (Pizza Hut).

As for Rakuten, the acquisition opens up a lot of opportunities in terms of connecting retailers and merchants with customers, particularly in order ahead and pickup.

“There’s a shift happening in consumer behavior where people want to save time. They want to order ahead on their mobile device and have things ready when they get there – whether that’s in the store or curbside in front of the store,” explains Waldman. “ARRIVE works really well in both use cases…And we’re also helping [retailers] really measure the performance of the individual store,” he says. “The folks that have that physical world touch point needs to ensure that stores are performing the consumers are actually not waiting that long.”

Rakuten today reaches over 1 billion members worldwide, including those on its own Rakuten Ichiba online marketplace in Japan.

Those online merchants could potentially take advantage of the Curbside technology to offer the option of order pickup for their customers, alongside their existing delivery options.

These sorts of integrations may not be limited only to the marketplace itself, however. Rakuten also has other consumer touch points, like communications app Viber and eBates.com, where Curbside could also reach the consumer audience in various ways. And it has investments in companies like Pinterest, Lyft, Cabify, and others, where it could do the same. It also has a partnership with Walmart in Japan in online grocery, where Curbside pickup could get involved.

In fact, Waldman says there are at least half a dozen opportunities inside Rakuten it could now pursue. The question is really which ones will it go after first.

“I can say there’s a ton of interest to bring this technology to Japan,” he notes. “They already touch 100 million consumers in Japan – their registered users. We could hook up this really big ecosystem of consumers and merchants,” adds Waldman.

He’s also excited to broaden the Curbside offering thanks to Rakuten’s expanded resources.

“We don’t have an out of the box payment solution. There’s a lot lot in the Rakuten ecosystem that’s going to allow us to to broaden that offering, which means that we can add more value for for our merchants and our retail partners,” he says.

And as a part of Rakuten, Curbside can more quickly expand to global markets – something it had just begun doing with smaller launches in Canada and India.

“Rakuten was founded on the philosophy of empowering merchants to reach consumers in new ways. In 1997 it was selling on the internet. Today it’s mobile commerce. Curbside has a unique ability to surprise and delight consumers with fun and convenient ways to shop while empowering local merchants,” says Yaz Iida, President of Rakuten USA. “It fits into our unique philosophy and will be a piece of Rakuten’s ecosystem of internet services.”

Curbside’s 60-person team, for the time being, will remain in its Palo Alto offices, though it may later move to Rakuten’s offices in San Mateo. Waldman remain as Rakuten Curbside CEO.

The startup had raised between $40 million and $50 million, including its undisclosed investment by CVS in 2016. Before that, it had raised $34.5 million, according to Crunchbase.

Stitch fix blows out Wall Street’s expectations and announces the launch of Stitch Fix Kids

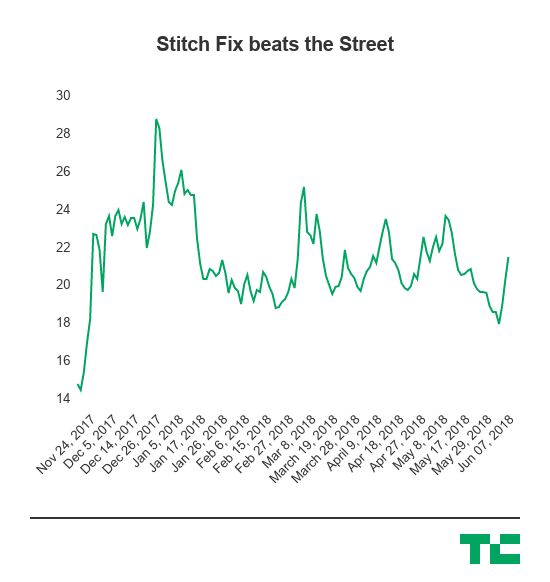

Stitch Fix, one of last year’s high-profile IPOs, has had a bumpy ride for the past few quarters — but it blew out expectations this afternoon for its most recent quarter, and the stock went absolutely nuts.

There’s also a ton of news coming out from the company today, including the hire of a new chief marketing officer as well as the launch of Stitch Fix Kids. All this is pretty good timing because the company appears to be cramming everything into one announcement that is serving as a very pleasant surprise to Wall Street, which is looking for as many signals as it can get that the subscription e-commerce company will end up as one of the more successful IPO stories. Shares of the company are up more than 14 percent after the release came out, where the company beat out expectations that Wall Street set across the board — which, while not the best barometer, serves as a somewhat public barometer as well as what helps determine whether or not it can lock up the best talent.

However, following the announcement, Stitch Fix’s stock came back down to Earth and is up around 4 percent.

Here’s the final line for the company:

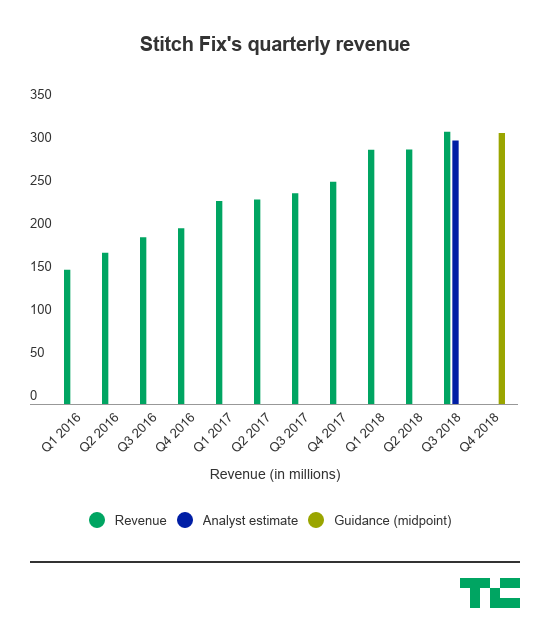

- Q3 Revenue: $316.7 million, compared to $306.4 million in estimates from Wall Street and up 29 percent year-over-year.

- Q3 Earnings: 9 cents per share, compared to 3 cents per share in estimates from Wall Street.

- Q4 Revenue Guidance: $310 million to $320 million, compared to Wall Street estimates of around $314 million.

- Cost of goods sold: $178.5 million, up from $139.7 million in Q3 last year.

- Gross Margin: 43.6 percent, up from 43 percent in Q3 last year.

- Advertising spend: $25.2 million, up from $21.3 million in Q3 last year.

- Active clients: 2.7 million, up 30 percent year-over-year (2.5 million last quarter).

- Q3 Net income: $9.5 million ($12.4 million in adjusted EBITDA).

Stitch Fix Kids will carry sizes 2T to 14, which will be across a diverse range of aesthetics “to give kids the freedom to express themselves in clothing that they feel great wearing,” the company said. Those Fixes will include 8 to 12 items that include market and exclusive brands. Stitch Fix launched Stitch Fix Plus in February last year.

“Our new Stitch Fix Kids offering is a testament to the scalability of our platform,” CEO and founder Katrina Lake said in a statement accompanying the release. “We’re excited for Stitch Fix to style everyone in the family and to create an effortless way for parents to shop for themselves and their children. Our goal is to provide unique, affordable kids clothing in a wide range of styles, giving our littlest clients the freedom to express themselves in clothing that they love and feel great wearing.”

Stitch Fix was widely considered a successful IPO last year, though it faced some challenges over the course of the front of the year. But as it’s expanded into new lines of subscriptions, its customer base still clearly continues to grow, and the company is still finding newer areas to expand — including the upcoming launch of Kids that it announced today. Like many recent IPOs, Wall Street is likely going to look for continued growth in terms of its core business (meaning, subscribers), but Stitch Fix is showing that it’s able to not set cash on fire as fresh IPOs sometimes do.

Stitch Fix’s new CMO, Deirdre Findlay, comes to the company from Google, where she oversaw the Google Home hardware products, which included Home and Chromecast. Prior to that, Findlay has a pretty extensive history in marketing across a wide variety of verticals beyond just tech, including working with Whirlpool Brands, Allstate Insurance, MillerCoors and Kaiser Permanente, the company said. While Stitch Fix is a digitally native company, it’s not exactly an explicit tech company and requires expertise outside of the realm of just the typical tech marketing talent — so getting someone with a pretty robust background like that would be important as it continues to expand into new areas of growth.

Zebra Medical Vision gets $30M Series C to create AI-based tools for radiologists

Zebra Medical Vision, an Israeli medical imaging startup that uses machine and deep learning to build tools for radiologists, has raised a $30 million Series C led by health technology fund aMoon Ventures, with participation from Aurum, Johnson & Johnson Innovation—JJDC Inc. (the conglomerate’s venture capital arm), Intermountain Health and artificial intelligence experts Fei-Fei Li and Richard Socher. Existing investors Khosla Ventures, Nvidia, Marc Benioff, OurCrowd and Dolby Ventures also returned for the round.

Zebra also announced its Textray research today, which it claims is the “most comprehensive AI research conducted on chest X-rays to date.” Textray is being used to develop a new product that has already been trained using almost two million images to identify 40 clinical findings. Scheduled to launch next year, it will help automate the analysis of chest X-rays for radiologists.

Founder and CEO Elad Benjamin, who launched Zebra with Eyal Toledano and Eyal Gura in 2014, told TechCrunch in an email that its Series C capital will be spent on new hires to speed up the development of its analytics engine and its go-to-market strategy.

Chest X-rays are one of the most common radiographs ordered, but also among the most difficult for radiologists to interpret. There are several groups of researchers focused on using artificial intelligence algorithms to make the process more accurate and efficient, including teams from Google, Stanford and the Dubai Health Authority.

Benjamin said Zebra, which has now raised a total of $50 million, differentiates its approach by looking at its algorithms from a “holistic product perspective. Developing an algorithm is just one piece,” he added. “Integrating it into the workflow, adapting it to the needs of multiple countries and healthcare environments, supporting and updating it, and regulating it properly globally takes a tremendous focus – and that’s what delivers value, over and above an algorithm.”

He added that “it will take a few more years” before AI becomes mainstream in medical imaging and diagnosis, but he believes that it will eventually be a critical component of radiology. Zebra Medical Vision already markets a bundle of algorithms for lung, breast, liver, cardiovascular and bone disease diagnoses called AI1 that costs hospitals $1 per scan.

In a press statement, aMoon managing partner Dr. Yair Schindel said “We are excited to partner with the Zebra team, which is harnessing the power of data and machine learning to provide physicians and healthcare systems with tools to dramatically increase capacity, while improving patient care. This investment aligns with our vision of backing scalable and sustainable innovations that will have a valuable impact on fundamental facets of global healthcare.”

Laka raises $1.5M seed to take its ‘crowd insurance’ model beyond bicycles

Laka, a London-based insurtech startup that offers what it calls “crowd insurance” to rival traditional premiums and is initially targeting high-end bicycle owners, has raised $1.5 million in seed funding. The round is led by publicly-listed Tune Protect Group, with participation from Silicon Valley’s 500 Startups — money that will be used to enter new insurance categories and for international expansion, including South East Asia.

Founded in 2017, Laka has developed what it claims is a unique insurance model that sees customers only pay for the true cost of cover. At the end of each month, the cost of any claims is split fairly between customers, with the individual’s maximum premium capped at the “market rate”. If there is no claim, the premium that month is zero. To date, the startup says it has saved customers more than 80 percent compared to market prices.

What’s interesting about this model is that it is potentially much-better aligned with customers, meaning that fewer claims mean lower costs for the entire Laka customer base. Laka itself only makes money when a claim is made — it adds 25 percent on top of each claim to cover costs and create some margin. As long as it stays on top of fraudulent claims, customers stand to benefit with a more cost-effective and fairer insurance product.

“Customers join without paying any upfront premiums. When there is a claim, we settle it with working capital we borrow from our insurance partner in exchange for a fee,” explains Laka co-founder Jens Hartwig. “At the end of the month, we total up all claims we have settled, add our fee on top, and split the bill on a pro-rata basis. Thus, we pay out first and then ask customers to pay us back the expenses incurred”.

In contrast, the more a traditional insurer pays out in claims, the less profit it makes. “It’s a great business model from the insurer’s point of view as they happily take customer’s money and maybe settle a claim down the line. In the meantime they can reinvest the available capital. This proposition is clearly not as attractive from the customer’s’ point of view,” says Hartwig.

To change this, Laka’s model moves away from “underwriting risk” to credit risk — that is, ensuring customers can pay the required, albeit capped premium when the startup does have to pay out, which Hartwig reckons is an easily manageable risk with credit cards and modern payment providers such as Stripe.

The cap — where the monthly premium has a maximum so that Laka’s customers never face bill shock — is being provided by Zurich U.K. in the form of a stop-loss agreement for which Laka pays a small fixed fee per policy, per month. Any exposure above the cap is absorbed by Zurich, acting like a reinsurer.

Hartwig says that in months with a lot of claims, this is where the stop-loss kicks in, capping each customer’s exposure at a clearly communicated level. The promise is that you will never be charged more than competitors, but — crucially — if everyone takes better care, you will pay much less.

“We effectively offer a profit share to our customers, encouraging improved behaviour as they benefit from taking better care. By changing the way we earn money in the business model, we fixed the conflict of interest between customer and insurer,” adds the Laka co-founder.

Source: https://techcrunch.com/

This user is on the @buildawhale blacklist for one or more of the following reasons: