Wharton FinTech Interview with Arthur Hayes, CEO and Co-Founder of BitMEX

TL;DR - originally published July 10, 2017

Podcast available here: https://soundcloud.com/wft/arthur-hayes-ceo-and-co-founder-of-bitmex

David Gogel chats with Arthur Hayes, CEO and Co-Founder of BitMEX, aka the Bitcoin Mercantile Exchange, a cryptocurrency-based derivatives exchange based in Hong Kong. They discuss Arthur's background, the launch of BitMEX, Bitcoin, Ethereum, derivatives trading, exchange business models, regulation, security, initial coin offerings, and the future state of cryptocurrencies.

BitMEX handles on average $100 million dollars per day in the total value of products traded. The company is wholly owned by HDR Global Trading Limited, a Republic of Seychelles incorporated entity.

Arthur Hayes, CEO and co-Founder of BitMexAfter graduating from Wharton, Arthur worked in Hong Kong as an equity derivatives trader. He was the market-maker for Deutsche Bank and Citibank's Exchange Traded Funds (ETF) businesses. He has extensive experience trading equity index futures, forwards, swaps, and non-deliverable FX forwards. He brings a deep understanding of how to structure / trade financial derivatives.

David: Hello, and welcome to the Wharton FinTech Podcast. I am your host, David Gogel, and I am joined by Arthur Hayes, the CEO of and co-founder of BitMEX. BitMEX, aka the Bitcoin Mercantile Exchange, is a cryptocurrency based derivatives exchange based in Hong Kong.

The company offers centrally cleared futures and swaps on Bitcoin versus fiat and other cryptocurrencies, also known as altcoins, with up to 100x leverage. BitMEX has partnered with experienced traders creating the most liquid derivatives exchange. The company is built by finance professionals with over 40 years of combined experience, and offers a comprehensive API and supporting tools.

BitMEX is now handling on average $100 million dollars per day in the total value of products traded. Welcome Arthur.

Arthur: Hi, thank you David.

David: So to start us off, can you tell us about your background and your career, [00:01:00] how you became interested in cryptocurrencies, and how you decided to launch BitMEX?

Arthur: I was a 2008 graduate of the undergraduate Wharton program with a concentration in finance. Like many of my classmates, I went into banking right after school. I studied abroad junior year and loved Hong Kong so much that I wanted to get a job there.

Luckily, I got a job at Deutsche Bank in the Hong Kong office, and I became an exchange traded fund market maker. For the subsequent five years, I was the head market maker for the Asia Ex-Japan / Australia Exchange Traded Funds (ETF) business for Deutsche Bank, and then Citibank.

In 2013, I was let go from my role as a trader, and I was looking for the next thing that I wanted to get into. I didn't really want to continue working at a bank. I [00:02:00] had read about Bitcoin when it had spiked to I think $250 in April 2013. I had some time on my hands. I started researching what Bitcoin was, was people were doing with it. And I went down a rabbit hole, and became very interested in this new currency and ecosystem.

Since 2013, bitcoin has surged in value….So much so, I decided to start trading it with my own money. I started trading arbitrage between the only futures exchange at the time called ICBIT [acquired by Safello] and Mt Gox [later filed for bankruptcy]. I did that for a while. I got into doing arbitrage between different spot exchanges for Bitcoin. And then I determined that I wanted to start my own derivatives exchange because I felt that the offerings at the time were not suitable for what I thought bitcoin and the whole industry would become.

I reached out to my network in Hong Kong, and I met my two other co-founders Ben Delo (COO) and Sam Reed (CTO). [00:03:00] Ben has a background as a high frequency trading technologist at some leading hedge funds and investment bank. Stan was a full stack web developer. In January of 2014, I pitched them the idea for BitMEX, and we decided to make a go at it. The rest is history.

The rest is history…

David: Let's talk about crypto derivative trading. Can you tell us more about what is Bitcoin, what are cryptocurrencies, what are derivatives, and what problems do they solve?

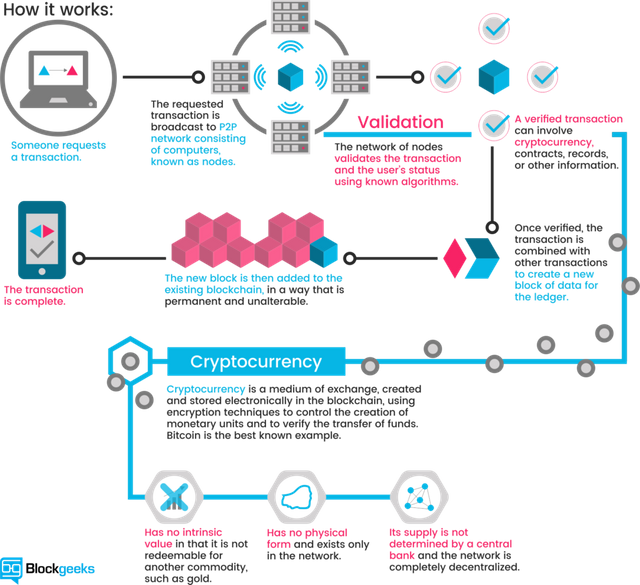

Arthur: Bitcoin, at a very high level, is a truly electronic form of money where the intrinsic value is essentially the usefulness of the Bitcoin network. It's a censorship resistant form of value transfer, meaning that there is no government or central bank that is telling you what the value of Bitcoin should be. It floats in a market just [00:04:00] like any other currency. And subsequently because of the innovation that Bitcoin has brought to digital money, there have been what's called altcoins, or other types of either digital tokens or digital currencies, mimicked on Bitcoin or mimicked on other applications.

When you move to the purely derivatives space, at the moment, the biggest use case for Bitcoin and other digital currencies is speculation. Once people [00:04:30] buy Bitcoin, they wonder what can I do with this Bitcoin. We're not at the stage yet where you can use Bitcoin to buy a cup of coffee or pay for a newspaper article.

Not yet but maybe soon?I think there needs to be competition in terms of decentralized money and the way value is transferred around the world, so I'm going to buy Bitcoin and hold it, and hope for appreciation in terms of a number of transactions, users, and the price of it itself.

Once people acquire Bitcoin, they then move up the ladder and they start [00:05:00] speculating on the future price of Bitcoin, and other digital currencies. And that's where BitMEX comes in. We use Bitcoin as a common form of collateral because number one it's programmable. We can take deposits and withdrawals 24/7 without any form of human interaction, and it costs us no money to onboard a customer. That's why we love Bitcoin as a form of collateral.

Once our customers have Bitcoin as collateral, we then offer them a full suite of financial trading products. And right now most of our products are centered around Bitcoin versus fiat currencies, like U.S. dollar or Japanese Yen, or another altcoin versus Bitcoin, like the Ether/Bitcoin exchange rate.

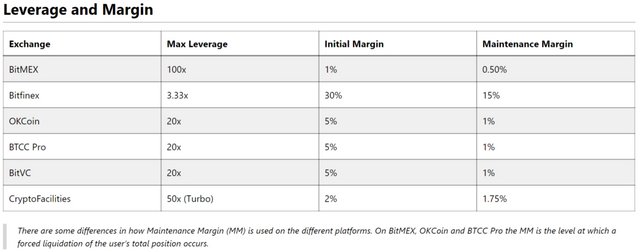

We offer traders the ability to trade with very, very high leverage, up to 100x on our most popular products. And so, I think as the market evolves, derivatives will be used more in a traditional sense for commercial hedging purposes, but right now [00:06:00] it's purely a speculation game.

David: You touched on this a little, but can you describe what your most popular product is today? what is your most popular contract type?

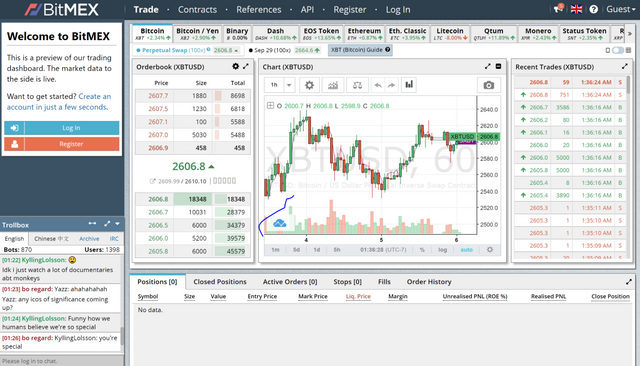

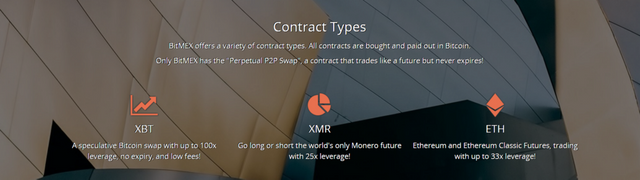

Arthur: Our most popular underlying is a Bitcoin/U.S. dollar product. And it's the most liquid trading product for the Bitcoin/U.S. dollar exchange rate globally. The structure of it is in the form of a perpetual spot. It's a combination of eight hour futures contract that can continuously rolls.

We invented this product to solve the problem that a lot of our clients who aren't very sophisticated in terms of trading financial derivatives, understand why a futures contract has to expire. To make the trading experience more robust for our retail customers, we created this product that doesn't have an expiry date. And to anchor the price of the product to the spot price of Bitcoin, we charge an interest rate between longs and shorts every eight hours.

That's where we came up with [00:07:00] the name for a perpetual swap. And this is our most popular product, and it creates anywhere $50 to $100 million U.S. dollars a day in trading volumes.

David: Today, is most of your customer base retail investors or institutional investors? In which countries are most of those investors based in?

Arthur: I'd say that 95% of our customers are retail. It's usually someone who has gotten into Bitcoin as I said, and has Bitcoin, and now they want to do something with it, and they start speculating with it.

The other 5% are ex-bankers who now act as market makers and liquidity providers. I would say that there is very little institutional presence in the Bitcoin space mainly because of the volumes. I think they're great now, but they need to be much larger for a large hedge fund or money manager to put significant amounts of money to work without impacting the market.

There's also issues around how do you store Bitcoin and the counterparty risk on exchanges. [00:08:00] So, we don't see that much institutional trading on Bitcoin, but obviously, interest given the recent price rise is picking up.

And then geographic location, right now the majority of our customers, or the biggest country is China followed by Western Europe. And right now what we're seeing in terms of where we see future growth, is South Korea. I think is going to be one of the largest trading centers for Bitcoin and other digital currencies, and Japan.

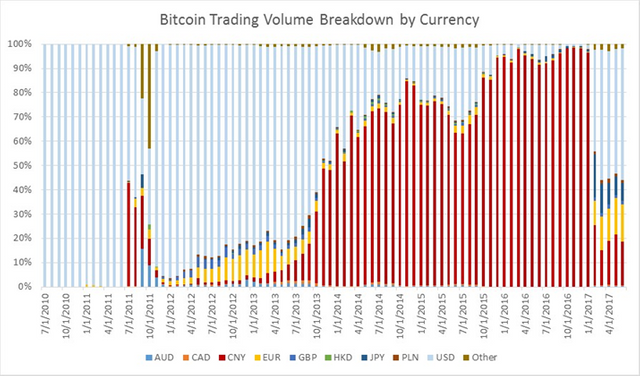

Notice Bitcoin volume shift from Chinese Yen (CNY / RMB) due to increase regulation in China explained below. Data from https://data.bitcoinity.org/markets/volume/all?c=c&r=month&t=bDavid: Who do you consider to be your peer set or your competitors?

Arthur: I mean, everyone's a competitor at the end of the day. It's kind of like a symbiotic relationship. We use exchanges for pricing, so obviously the underlying price. But we also compete for trading volumes because once you've gotten Bitcoin, we don't confuse any exchange, cash, or Bitcoin. But once you have Bitcoin, if you want to trade in and out, you can use a derivative, or you can use margin, or you can just go in and out of [00:09:00] cash with Bitcoin. It's kind of like we're competing for mind share of traders, and how's the best way to get that exposure that they would like. We're competing with everyone and working with them at the same time. We're all "frenemies" I guess.

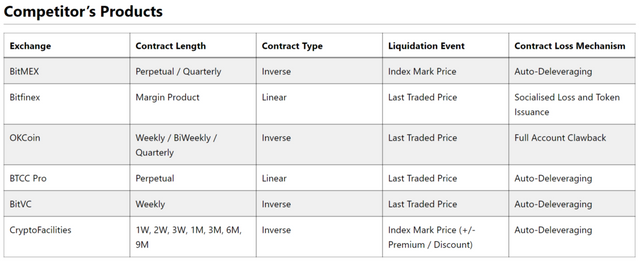

David: Are there other cryptocurrency derivatives exchanges, or are you guys the largest one?

Arthur: OKCoin is our biggest competitor in China. And then other than that, there's no one else that comes anywhere close to our volumes.

David: Given the recent rise in price of Bitcoin and other altcoins, have you seen volume shift away from Bitcoin options and swaps to other altcoins, or is the majority of your volume still concentrated in Bitcoin derivatives?

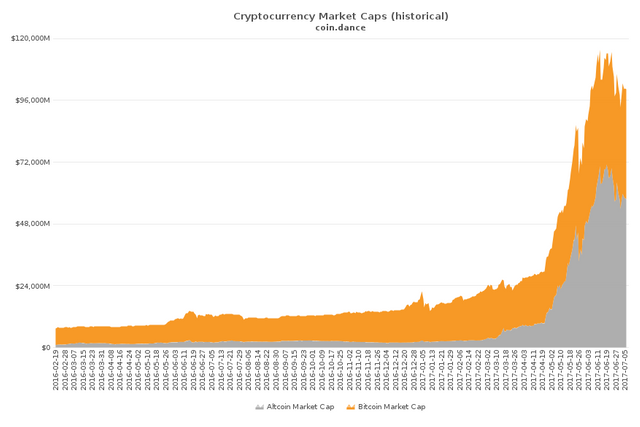

Arthur: For BitMEX, the majority of our volume is concentrated in Bitcoin, but if the market as a whole, given the recent surge in the price of Ethereum, I would say that Ethereum now trades greater volumes than [00:10:00] Bitcoin. At least reported volumes on exchanges.

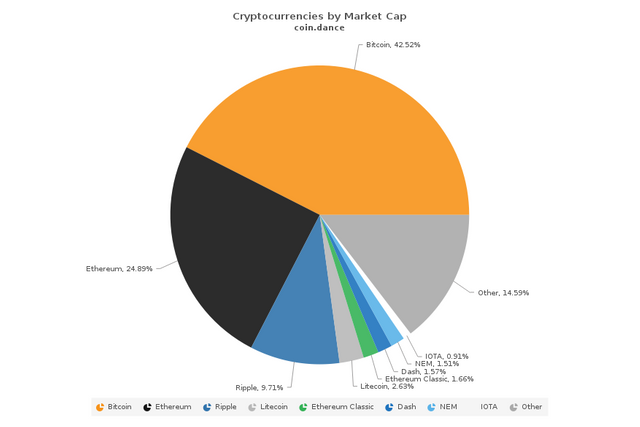

Now that we're moving into a post Bitcoin world, where you have all these other currencies gaining significant traction in terms of market caps and price, we're going to see much more competition between the different tokens and currencies, depending on what they claim to be used for.

David: From an exchange business model perspective, can you talk about how BitMEX differentiates itself relative to other cryptocurrency exchanges, like Coinbase, that people in the U.S. have heard of?

Arthur: BitMEX is purely a contract exchange. We do not engage in the activity of exchanging a fiat currency for Bitcoin, or changing Bitcoin for another digital token or another digital store of value. That's where we are probably one of the only exchanges [00:11:00] if you want to call it that, that only deals in contracts, or derivatives.

And then in terms of our business model, it's very simple. We charge a transaction fee every time a user trades our product. This nets out to about 0.05% is the fee that we charge to trade our product.

David: 100x leverage is obviously a lot of leverage. Structurally, how are you able to offer that much leverage to your customers?

Arthur: The first thing is that we built our entire exchange using the kdb+(database) technology, column-store database programming language. It's used by basically every large investment bank and high frequency trading hedge fund.

This technology enables extremely fast processing speed. And we can do large amounts of number transactions and do them correctly. Some of the other programming languages that many exchanges [00:12:00] use are not suited for high frequency trading of any type of assets. So, that's the first thing.

And because we built our exchange in a very generalized manner, and to scale, we're able to offer large leverage. The big problem with leverage is that a small move in the price will generate liquidations from clients. And those liquidations need to be cleared extremely quickly, otherwise we get cascading margin calls and other situations.

No one wants margin calls…And we don't want customers trading at very off-market prices. It looks bad for the exchange, it looks bad for the industry as a whole. It's really a technology issue that we're able to offer the highest leverage and speed in the Bitcoin industry.

David: Have you faced any issues scaling your business with the recent rise in price and volume of cryptocurrencies? Have you faced any issues with getting new customers on board or opening up accounts?

Arthur: [00:13:00] Because we do not handle fiat money, our client onboarding process is absolutely autonomous, and it's automated. The client, all they need is a verified email address, they sign up, verify their email address, then they're presented with a Bitcoin address. They can deposit Bitcoin, and within one network confirmation, which is about ten minutes, they can begin trading. That process requires no humans.

You can juxtapose that to a traditional exchange, like you said Coinbase or Kraken, where if you want to send them your U.S. dollar, Euros, or whatever currency, that needs to go through the banking system. And obviously there are delays. Somebody might have put the wrong instructions on the transaction, which generates a lot of friction for setting up customers, and it generates a lot of support tickets.

We have been totally fine with the surge interest and our current onboarding process has not been affected. In terms of our trading technology. as I said, [00:14:00] we built it with industry standards tech that has allowed us to scale with no issues. In 2016, we had a total of one minute of down time, over 365 trading days, 24 hours a day. Our trading technology is, in my opinion, the best in the cryptocurrency industry.

David: Wow, that's a really impressive statistic. What types of investors are eligible? You guys aren't technically part of the banking system. Can you be an American [00:14:30] citizen and buy or transact via BitMEX, or do you only focus on non-U.S. based customers?

Arthur: We only focus on non-U.S. based customers. It's purely a regulatory issue. I'd say that for any of our competitors, I don't think there are any Bitcoin based derivatives platform that offer products to U.S. customers.

David: Do you see the U.S. regulatory environment becoming more favorable when it comes to cryptocurrencies, and altcoin trading in the future? Do you think that most of the development is going to continue to occur offshore?

Arthur: I think that the U.S. will lag behind in terms of the breadth of products offered for digital currencies, trading volumes and innovative nature of the companies. Mainly that's because the U.S. is intent on applying banking regulations to essentially an industry filled with startups. If you look at the exchanges in the U.S. who are able to comply, they've raised hundreds of millions of dollars to do that. They're focused on pleasing regulators, and not pleasing their customers.

Whereas you come out to Asia with much more my guess easier or there's more allowance for new ways of doing things because in some cases a traditional banking system doesn't really work for the country. Then you [00:16:00] get much more innovation. And that's why you see the largest trading lines in China, South Korea, and Japan, not in the U.S.

Venture capital deal share by country

David: We talked about trading volumes out of China earlier in our discussion. How exposed is your business model to regulation in China around cryptocurrency flows? And have you thought about any ways to diversify your portfolio of products away from Chinese renminbi denominated transfers?

Arthur: As [00:16:30] I've said, we don't handle cash, so technically we don't exist in China. We're an offshore company. Someone has to have Bitcoin before they can trade on BitMEX. Which essentially means they're going to have to go through whatever the KYC annual policies are for relevant exchanges onshore in China.

We're not a party to any possible people evading capital controls. If you deposit Bitcoin on BitMEX, you can't turn it into U.S. dollars, and then wire that out to another bank [00:17:00] account. We're not really a conduit for all of that. A lot of the things that the PBOC, People's Bank of China and the central bank, have been focusing on is around making sure the provenance of renminbi (RMB) is accounted for properly by exchanges. Now that's not really our business, we don't allow people to give us renminbi. We don't do any sort of transfers.

We're not really exposed to regulatory risk per se in China. What we have seen [00:17:30] is that the regulators have been very permissive of Bitcoin trading. PBOC did not shut down Bitcoin trading earlier this year. They just put some roadblocks in place to make it conform to a more normal exchange operation. Like the removal of leverage, the mandation of trading fees, the upgrade of the KYC and AML policies of the large exchanges. And then after about three months, they then allowed them again to process Bitcoin withdrawals.

[00:18:00] Trading in China for Bitcoin, while the volumes are down because there's no more margin trading onshore, and they had to remove the free trading, there's still significant amount of interest in China. And with the phenomenal number of people in China who have Bitcoin, and know what the coin is, is much larger than anywhere else. It's still a very exciting place for digital currencies.

David: Overall, what do you think it will take for more institutional players to enter this market? Do you see a potential future where people are trying to hedge their portfolios using Bitcoin derivatives? What's that threshold that you think would be required for the big players to enter this space?

Arthur: The first thing is I think that a large institution, or a large money manager, needs to be comfortable with the counterparty risks of the exchanges. So, unlike a regular retail investor who might just buy some Bitcoin and hold it in their own personal [00:19:00] wallet, if you are in the trading business, you're going to have to hold Bitcoin and other digital currencies on the actual exchange so that you can transact. And that opens yourself up to the exchange getting hacked, the exchange stealing your money, or all the other issues that exchanges face in the industry.

The trading opportunity in terms of the amount of money they can make from this has to be sufficiently large enough so that they are willing to take that risk. Now, as the trading volumes have skyrocketed this year, and the total industry has over a hundred billion dollar market cap, I think that question has become easier to answer. Institutions are getting warmer to the idea of holding Bitcoin on these exchanges.

And then, just in general, the trading volumes still need to get larger. I don't foresee a Goldman Sachs trading desk transacting in Bitcoin yet, because they can't make enough money to move the needle, to be worth all of the issues that they have to face trading Bitcoin, learning how to store it properly, possible [00:20:00] regulatory issues because as I've said, the majority of the volume is not on U.S. regulated exchanges. This is one of the issues that the SEC [Securities Exchange Commission] noted in their recent disapproval of the Winklevoss coin ETF. That is I think some of the bigger issues. Now a smaller firm, a prop shop, they are getting more interested in the trading Bitcoin. And some of them have sticked their toes into actually market making and putting on certain strategies [00:20:30] in Bitcoin.

I definitely can see a future where a firm like Jane Street, Susquehanna, those type of firms will get involved and trading Bitcoin well ahead of say a CalPERS, or a large investment banking and trading desk, providing markets and/or doing proprietary trading.

David: You mentioned the Winklevoss Coin ETF. I know there's been a lot of interest in the U.S. recently in Bitcoin denominated, or Ethereum denominated [00:21:00] ETFs. Do you see that as a potential entry point for large institutions to also get exposure the market in the future?

Arthur: I think the ETF will be a game changer for Bitcoin. Depends on which country lists one first. Obviously the SEC sort of punted that decision. It's unclear what the timeline will be for another possible bid, where they could approve an application. Now I think there are some [00:21:30] players working on an ETF, which is in Europe, possibly getting a UCITS certification. I'd say either U.S. or Europe, if there is a traditional wrapper where a retail investor can eventually log onto their stock trading account and just click, and get some Bitcoin exposure, the liquidity is going to dwarf the actual underlying exchanges, which will obviously lead to a spike in the price.

And then traditional asset managers [00:22:00] can then market make an ETF, they can get exposure via the ETF, and they never have to touch Bitcoin. Now, obviously it puts the trust on the fund manager to properly secure all the Bitcoin assets, but if they're comfortable that the regulators approving their application did proper due diligence, then that concern should melt away, and you'll see a shift of a lot of trading volume on ETF type derivatives listed on exchanges.

Now, right now in I think Stockholm, there's an exchange traded note, an ETN, that takes the credit risk of issuer. It's not an ETF per se. However, that ETN is doing very well in terms of trading volume. And the firm that owns that ETN is called GABI (Global Bitcoin Advisors) run by Daniel Masters and a few other experienced commodities traders. They are trying to get a properly listed ETF in Europe.

[00:23:00] I think the U.S. avenue is probably closed for a year to two years. But, I looked to Europe for this one first.

David: In the past several crypto exchanges have been hacked, and coins have been lost, can you talk a little bit about how BitMEX ensures maximum security on the funds that it holds?

Arthur: Yes, listeners should understand one concept, what we call a hot wallet. A hot wallet basically means that there is private keys, or the ability to send [00:23:30] Bitcoin on a server connected to the internet. And so, let's say that I loaded a hundred U.S. dollars on Coinbase, I buy some Bitcoin, and I want to withdraw that Bitcoin immediately to my own personal wallet.

The exchange does this programmatically and automatically using a hot wallet, to authenticate your withdrawals, and then the server will send you back via the transaction, and send Bitcoin automatically. Now, exchanges usually keep 1-5% of their [00:24:00] total deposits that they have in a hot wallet. And because it doesn't require human oversight to send Bitcoin, this is the preferred way for hackers to steal Bitcoin from exchanges.

In 2015, early 2015, Bitstamp lost five million U.S. dollars, due to a breech in their hot wallet. BitFinex lost a few hundred thousand dollars in the same year due to a breech in their [00:24:30] hot wallet. And multiple other exchanges usually are hacked through a breech in their hot wallet. Now, that's contrasted to what we call a cold wallet. Usually that's where the private key is stored on a piece of paper. It's printed out and stored in a bank security deposit box. And to access those Bitcoins, requires a human to physically get that piece of paper, load up a Bitcoin wallet, and then physically sign a transaction.

So, that's the most secured method because [00:25:00] the Bitcoin private keys are not connected to the internet. The first thing that BitMEX does, is we're a derivatives exchange. Our clients don't expect to have immediate access to their Bitcoin. Our first policy that we enacted is there will be no hot wallet. We only do withdrawals once per day. And all those withdrawals are done manually by a two out of three of the co-founders.

Now we used a wallet technology called Multi Signature, which basically means M of N signatories [00:25:30] need to authenticate a transaction before it can be broadcast to the network. We have a process around this. And because it's manual, we only do it once a day. Because we only do this once a day, it allows us to check outgoing Bitcoin from BitMEX.

A lot of times we'll message customers who are withdrawing large amounts of Bitcoin, especially to addresses they haven't sent to before, of if they don't have two factor authentication enabled. [00:26:00] This has enabled us to date to have no incidents of us being hacked, or someone getting access to customer's Bitcoins.

And if somebody wanted to take down the BitMEX website, there are no private keys on the internet. DDoSing our exchange, and maybe getting access to some private keys, is not going to happen at BitMEX. And so that is how we have minimized the threat to our Bitcoin wallet.

David: Shifting gears a little, are there any developments in FinTech broadly that are particularly interesting to you? In the U.S., there's been a recent interest in ICOs, Initial Coin Offerings. Do you see an opportunity in the future for BitMEX to support derivatives trading on these types of altcoins?

Arthur: We think the ICO market is the revolutionary way of raising money from a large amount of people without a large amount [00:27:00] of overhead. For an Initial Coin Offering, the major difference between that and the traditional IPO is you're not buying equity in a company per se, but you're buying rights to use a decentralized application in most cases.

So, the tokenization of companies allows them to access the world's capital markets, the 90% of people who will never participate in the equity markets, or the private markets, and get a small amount of money from a large number of people, and essentially bypass the traditional [00:27:30] venture capital / private equity model of raising funds for a new venture.

While traditional VC investment deals to private blockchain companies rose for the third consecutive quarter, more of these startups are turning to initial coin offerings (ICOs) as a viable financing method. Still shaky from a regulatory perspective, ICOs are token sales offered by blockchain companies looking to exchange equity for financing. Tokens are subsequently traded on cryptocurrency exchanges, and rise or fall in value as a function of the company's popularity, growth potential, and/ or general speculation, similar to conventional securities and liquid markets. This is extremely powerful for teams of developers. If you could produce an asset will have a use case, and will be used, you can sell the right to use those applications directly to your customers. Not only do your customers get the benefit of using your applications, they are also incentivized because they basically own a piece of it to tell their friends about it, get more people to use it, so that this token [00:28:00] that they have bought has a value because the underlying application that it's made into is used.

Now at BitMEX, we think this market is right for using derivatives to bring a market discovery. So usually what happens is a team will have an ICO. It'll last for a period of time. And then there will be sort of like a blackout period. You subscribe for the ICO, and you'll know you'll get your token in say a month, or two months, or three months. But in that period, there's no signal as to what the value of that token should be.

A lot of times these projects are in the preliminary stages of launching. So, there'll be developments in terms of going behind schedule, or maybe they got a new partnership with a large player. And it will affect the perceived value of this token.

What we do is we launched a Bitcoin margin futures contract on ICO tokens before they list on the secondary market. This allows [00:29:00] people who want to lock in possible gains from the project mission period until now. They can sell these futures contracts, and go short. And all they have to do is pledge Bitcoin. And on the long side, people who have missed out on the ICO, because a lot of these things are sold out within seconds, are able to purchase a derivative and gain economic exposure to the ICO before it lists on a secondary market.

I guess the biggest one we've done so far is Zcash, and that was last year. We launched a futures contract on Zcash versus Bitcoin before Zcash began mining. And so people were able to speculate on what the value of Zcash versus Bitcoin would be three months after the genesis block. And we aimed to replicate that with other large tokens.

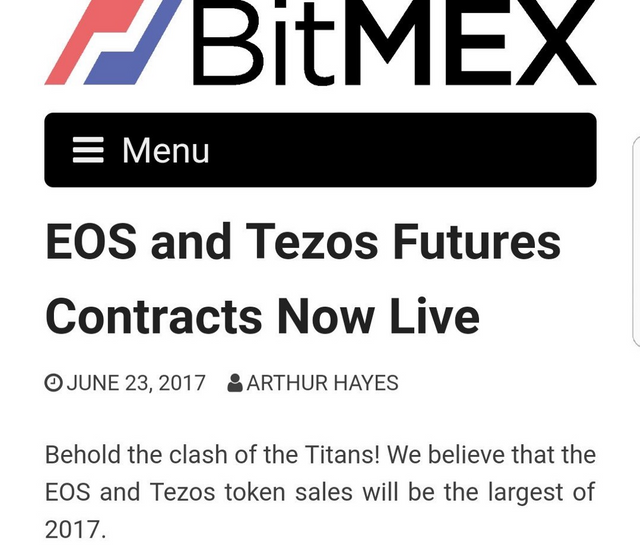

So right now, we have a Tezos ICO contract, which is another large deal. I think they've raised them $200 million [00:30:00] so far. We have a contract on EOS, which is another protocol that has just launched. I think they've raised two or three hundred million U.S. dollars so far. It's becoming a preferred way for speculators and hedgers to gain exposure on the long or short side to a particular ICO.

David: Do you plan to expand your ICO derivatives product to all ICOs, or how do you evaluate which ICOs [00:30:30] are worthwhile versus others that may be less worthy?

Arthur: I guess it's a little bit like hot or not. We only like to list ICO futures contracts on the controversial deals. Usually they're controversial because either it's super shady and people think that these guys are scamming, and they've gotten a lot of money. We give people the opportunity to go short. Or the deal is so large it attracts interest.

Tezos [00:31:00] and EOS have both combined raised close to half a billion dollars. The implied market cap of these coins is multiple billions of dollars. So sufficiently large to generate interest from our traders.

We don't generally deal with smaller deals, sub-half a billion dollar implied market cap because you can get considerable interest from our traders.

David: Have you guys raised any financing or funding?

Arthur: No. We basically did some family and friends [00:31:30] in 2015, and then we got profitable, so we didn't really need to raise any money. We own most of the company, well, you know, the vast majority of all the shares. And we're profitable, so we don't really need to raise any money, which is a good place to be.

David: Have you ever considered launching an ICO for BitMEX?

Arthur: We thought about it, but the issue is we don't really know, we are a little different because most ICOs is… I built this protocol, or application, and [00:32:00] I'm selling a token and half of it is used on that app. It doesn't have any equity rights, it doesn't have a cash flow stream. So if we did an ICO, the only way to really get people to buy it, is if they get a piece of BitMEX, or they get some sort of trading revenue dividend.

And once you do that, then it's a security. And then depending on what country people buy this thing from you off of, then that's an unlicensed security. Unless you go through particular processes. It takes away all the sexiness of an ICO, because the sexiness is here's a website, here's an address. If you want to get in, send some money, and we're gong to sell you this token that doesn't have any value unless what we built is actually useful to the wider community.

You see very few security like ICOs because number one, the upside isn't that big, so yes, buying equity into the company you can make some money, but buying into the next Facebook-like application for [00:33:00] the crypto space, is much bigger. So people like to invest in those. They don't like to invest in something that they can actually model and touch your life, and okay. Here are the cash flows. I can apply a multiple to it, here's the value, and then we're going to end up … Those ICOs never do well because the people don't want that. They want the next Facebook, the next Twitter, the next Snapchat, which are unprofitable, very risky ventures with no ability to attach a traditional DCF or comp multiple on.

David: If we take a step back and think through where the overall cryptocurrency market is going to be in maybe five or ten years, what's an ideal end state? And where do you see BitMEX operating in the future?

Arthur: I think the question that many people are asking now is this a bubble, or will we continue?

And really, it's a question of will high net worth individuals, you know people worth over probably a hundred thousand dollars of liquid assets, will they [00:34:00] put a small percentage of their net worth into the digital currency ecosystem. If you believe that's going to happen because of increased awareness due to the amazing price rises over the last two years, then a hundred billion dollar market cap is going to be eclipsed quite soon. We could be approaching one trillion dollars within one to two years.

In terms of an end game, I think that there will be a token for every type of online application. [00:34:30] There will be different currencies with different communities that are truly a digital space. And there will be one king, sort of the digital gold, sort of the reserve currency for the decentralized world purely on the internet. Right now, that looks like it's going to be Bitcoin, but there will definitely be other challenges to that.

At BitMEX, we're agnostic to which digital currency or currencies become the most widely held and traded. We just take [00:35:00] a currency as a common form of collateral. We just want to be able to service the most amount of customers and offer them products at a very low price, and be able to onboard them essentially for free.

We see ourselves as being a place where anyone, anywhere can trade any type of financial asset. As long as they can provide a suitable form of decentralized money to us as collateral. And so we aim to get into using Bitcoin as collateral to trade traditional assets. Later end this year, we will offer a equity total returns swap that is collateralized in Bitcoin, and give certain jurisdictions in the emerging world the ability to buy and hold a synthetic share of a U.S. company, and invest, and get access to traditional products that they might never be able to access using their traditional domestic currencies.

And so essentially at an end, we are sort of like a crypto investment [00:36:00] bank, but we don't cater to our high net worth, we cater towards retail investors or those who have been traditionally left out of the financial industry.

David: Do you have any tips for FinTech enthusiasts / Wharton entrepreneurs who are interested in getting more involved in the cryptocurrency space?

Arthur: First thing is, take an amount of money that you can afford to lose, and experiment with buying and selling Bitcoin, or Ethereum, or some other of these digital tokens. Get your own digital wallet, play around with it, send money to your friends. See the different types of services that are offered. And then if you really want to get into this space, start going to local meetups in wherever you are based.

Everyone in this industry is very friendly because it's still super small, even though in 2017, there's been a lot of good press about Bitcoin, Ethereum, and other applications. We're still just scratching the surface of what this can do. So everyone is very [00:37:00] incentivized to talk to many people and get them in the industry, especially people from a very, well regarded MBA program like Wharton. I think that it'll definitely open doors. Go to the meetups, stay interested, and you will definitely be able to grab coffee or grab a Skype call with any of the leading figures in the industry.

David: There's a huge interest in cryptocurrencies in the U.S. these days. And even at Wharton, we've a huge surge in the last two or three months of people really interested in this space. This is like way more advanced. I think people are still trying to grasp the concept of what's a cryptocurrency, what's an ICO…

Google Trends interest over time for "bitcoin"And the fact that you guys are already operating the derivatives space is pretty amazing to see how liquid this market is already. Post the recent surge, the SEC is getting a lot of pressure from some big hedge funds to try to allow an ETF [00:38:00] of some sort to be registered in the U.S.

It is kind of an arms race between Europe, the U.S., Asia in terms of who wants to be known as the leader when it comes to innovative cryptocurrency startups. I know Coinbase for example announced they're trying to raise at a billion dollar valuation. And there's been some rumors that they may start to offer derivatives contracts, if the SEC allows them to do it.

Arthur: I mean, it'd be great. I hope that there are more offerings or derivatives. It [00:38:30] increases liquidity, increases interest, and allows more trading to happen. I think the CME (Chicago Mercantile Exchange) is going to have a futures contract for Bitcoin by middle of next year [2018]. There's definitely going to be some sort of U.S. based derivative approved for high net worth clients. Can't wait for that to happen. It's going to be great for everybody.

David: That concludes today's podcast. Thank you so much Arthur. We look forward to [00:39:00] seeing BitMEX continue to be successful, and pave the way in the cryptocurrency market. Thanks again.

Arthur: Thanks for having me on. Thanks a lot.

Disclosure: I have no positions in any cryptocurrency derivative contract on BitMEX. I am an investor in Bitcoin and Ethereum, and several other tokens / ICOs. I wrote this article myself, and it expresses my own opinions. Wharton FinTech is not receiving any form of compensation.

Coins mentioned in post:

✅ @dgogel, I gave you an upvote on your first post! Please give me a follow and I will give you a follow in return!

Please also take a moment to read this post regarding bad behavior on Steemit.

Congratulations @dgogel! You have completed some achievement on Steemit and have been rewarded with new badge(s) :

Click on the badge to view your Board of Honor.

If you no longer want to receive notifications, reply to this comment with the word

STOPCongratulations @dgogel! You received a personal award!

Click here to view your Board of Honor

Congratulations @dgogel! You received a personal award!

You can view your badges on your Steem Board and compare to others on the Steem Ranking

Vote for @Steemitboard as a witness to get one more award and increased upvotes!