마이테이타 데이타표준, 오픈뱅킹 API 그리고 ISO 20022

1.

최근 금융위워회가 지급결제와 관련한 정책을 잇달아 발표하고 있습니다. 금융결제 인프라 혁신 방안을 시작으로 금융분야 마이데이터 산업 도입방안및 신용정보산업 선진화방안이 관련한 정책입니다. 이상의 정책은 관련한 해외정책, 특히 PSD2와 같은 정책을 분석하여 한국에 적용한 것입니다. 보도자료에 첨부한 정책자료를 꼼꼼히 읽어보면 Open API가 자주 등장합니다.

지급결제와 관련한 Open Banking API가 있고 마이데이타를 위한 데이타표준 API가 있습니다. 저는 한국형 오픈뱅킹과 금융결제망 개방를 쓸 때 금융결제망을 강조하였지만 관련한 자료를 보면 오픈뱅킹 API를 2단계로 중요하게 다룹니다.

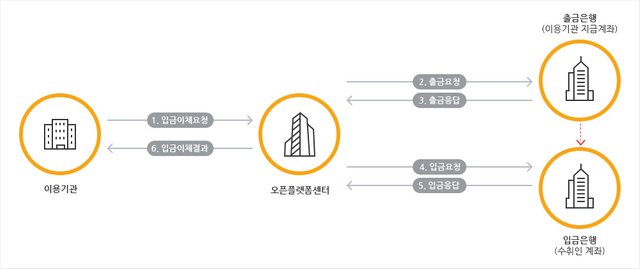

2단계에 추진하는 오픈뱅킹 API가 현재의 오픈뱅킹 API와 어떻게 다른지를 알아보려면 현재의 트랜잭션흐름을 이해하여야 합니다. 금융결제원이 개발 운영하고 있는 은행권 공동 오픈플랫폼에 올라온 흐름도입니다.

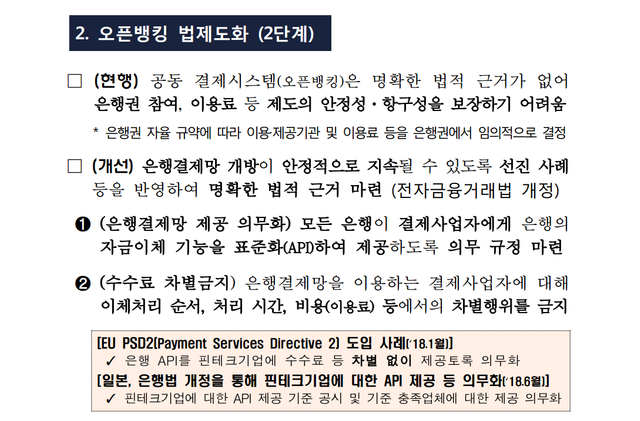

2단계중 "(은행결제망 제공 의무화) 모든 은행이 결제사업자에게 은행의 자금이체 기능을 표준화(API)하여 제공하도록 의무 규정 마련"와 비교를 하면 차이를 이해할 수있습니다. 현재는 금융결제원을 통하여 은행에 접속하는데 2단계는 Open API를 통하여 은행시스템에 접근합니다. 3단계는 은행을 통하지 않고 지급결제처리를 할 수 있는 소액결제망에 접근할 수 있도록 하였습니다.

지금결제와 관련한 API를 다룰 때 자주 등장하는 표준이 ISO20022입니다. ISO 20022은 2009년 제정한 국제표준으로 "금융업무 전반에 이용되는 통신메시지에 관한 국제표준으로 은행, 증권, 보험 등의 금융기관및 개인, 기업, 증권거래소, 청산소, 지급결제 관련 IT업체, 중앙은행, 감독기관 등 매우 다양한 형태의 참가자들 사이에서 이용되는 수많은 형태의 통신메시지를 ISO 20022 표준 체계 내로 수용하한 국제 표준"입니다. 처음 제정되었을 때 한국은행이 번역해서 발표한 ISO 20022의 주요 내용 및 대응과제에 아주 자세한 내용이 나옵니다.

[gview file="http://smallake.kr/wp-content/uploads/2019/05/ISO20022의-주요-내용-및-대응-과제.pdf"]

물론 ISO 20022과 오픈뱅킹 API가 직접적인 관계는 없습니다. 오픈뱅킹 API가 발전한 유럽에는 PSD2 규제하세어 다양한 오픈뱅킹 API 들이 존재합니다.

- Open Financial Exchange (OFX): OFX is a leading bank standard for financial data access, traditionally relying on user’s login credentials to access financial data. OFX is deployed at over 7,000 financial institutions and is used by providers such as CheckFree, Intuit, and Microsoft to support financial data exchange. The OFX Consortium released OFX Version 2.2 for comment in July 2016. OFX Version 2.2 supports OAuth tokenized authentication, supporting API access to financial data. The Consortium includes founders CheckFree, Intuit, and Microsoft along with Xero, Finicity, Silicon Valley Bank, and others.

- Durable Data API (DDA): An industry working group from the Financial Services Sharing and Information Sharing and Analysis Center (FS-ISAC) released DDA in May 2015. This working group comprised several financial institutions as well as a small number of financial data third parties. DDA was intended to improve data exchange relative to OFX[1]. Fidelity Investments and other large financial services firms have adopted the DDA standard for data sharing.

- NACHA API Standardization Industry Group (ASIG): The AISG is working to standardize the use of APIs in the U.S. financial services industry by creating an “API Playbook” or standards framework. The group has identified 16 APIs that it will develop to support payments industry advancement in the areas of Fraud and Risk Reduction, Data Sharing, and Payment Access. Group participants include banks, credit unions, solution providers, and central bankers.

- UK Open Banking Standard: Open Banking has created 8 APIs for consumer and business current accounts, SME loans, commercial cards, ATM locations, and branch locations. Open Banking does not provide direct access to live API endpoints. Rather, these are implemented and supported by each API provider. The API Dashboard lists all available API endpoints, and show which API version is supported by each provider.

- The Berlin Group NextGenPSD2: The Berlin Group is working on a detailed 'Access to Account Framework' with data model (at conceptual, logical and physical data levels) and associated messaging, based on the EBA Regulatory Technical Standards (RTS). A list of participating banks and service providers can be found here. The draft specification is targeted to be published for consultation in Q4.

- CAPS (Convenient Access to Payment Services): The CAPS market initiative is a large multi-stakeholder coalition that proposes solutions to the technical, business and operational issues faced by potential PSD2 stakeholders across Europe. Banks, TPPs, Fintechs, service providers, corporates, and other financial industry stakeholders are working together here to develop a framework. That said, participants are primarily solutions providers.

- OpenID Foundation Financial API (FAPI) Working Group: The FAPI WG aims to provide JSON data schemas, security and privacy recommendations and protocols to: 1) enable applications to utilize the data stored in the financial account, 2) enable applications to interact with the financial account, and 3) enable users to control the security and privacy settings. Both commercial and investment banking account as well as insurance, and credit card accounts are to be considered. A working draft of FAPI’s Open Data specifications can be found here.

이중에서 영국 UK OpenBanking이 만는 지급결제 API를 참고로 소개합니다.

[gview file="http://smallake.kr/wp-content/uploads/2019/05/DZ-PaymentInitiationAPISpecification-v3.1.2-170519-0216.pdf"]

이중 NACHA가 발표한 API Standardization - Shaping the Financial Services Industry를 보면 ISO 20022와의 호환성을 고려하여 API을 제정하였다고 합니다.

When payments are interoperable, they allow two or more infrastructures, platforms, and/or different products to interact seamlessly, enabling faster, more efficient and transparent transactions across disparate systems. Interoperability is significant because it permits customers to make payments in a convenient, affordable, seamless and secure manner. Having interoperable payment services allows customers to use the infrastructure of multiple regions and service providers to access their accounts, expanding the reach of transaction accounts and payment instruments, making them more useful for end users.The benefits of interoperability do not exist solely for the customer. Interoperability helps platforms and other ecosystem stakeholders to create better products in a more cost-effective manner, mitigating the impact of potential external constraints such as inaccessible payment infrastructures; enabling more efficient market conditions that market participants and overarching stakeholder communities desire; and facilitating easier access to payment instruments and transaction accounts. A key component of the API Standardization Industry Group’s strategy is to ensure interoperability and harmonization with these initiatives around the world to support domestic and global needs of industry stakeholders. This is achieved by working in collaboration with other industry standards bodies domestically and globally to promote interoperability. The API standardization efforts include mapping of the work efforts to ISO 20022 and leveraging the ISO 20022’s data dictionary where possible.

[gview file="http://smallake.kr/wp-content/uploads/2019/05/707-18-4-API-Standardization-Shaping-the-Financial-Services-Industry.pdf"]

한편 XMLdation은 ISO 200222를 이용하여 API를 구축할 수 있다고 말합니다.

이상의 논의를 통해 Open Banking API는 표준적인 Data Dictionary를 전제로 하고 ISO 20022이 정한 데이타사전을 기반으로 할 수 있습니다. 국내 오픈뱅킹 API와 관련한 2단계는 은행이 주도권을 가지고 알아서 만들어 제공하는 방식을 취할 듯 합니다. 그렇지 않으면 굳이 마이데이타를 위한 별도의 데이터표준API를 만들 이유가 없기때문입니다. 금융위원회가 발표한 데이터 표준 API」워킹 그룹(Working Group)을 구성·운영하여 금융분야 마이데이터의 조속한 정착을 지원에 담긴 데이터 표준 API 계획입니다. 전 산업의 표준화를 위해서라면 ISO 20022를 기반으로 하여야 하지않을까 생각합니다.

■ 금융분야 마이데이터 도입을 위한 「신용정보법」 개정에 미리 대비하고, 데이터 기반의 금융혁신 내용을 보다 구체화하기 위해ㅇ 정부, 유관기관(금융보안원·신용정보원 등), 주요 금융권, 핀테크업계 등의 실무자가 함께 하는 「데이터 표준 API」 워킹그룹(WG)을 구성·운영

■ 「데이터 표준 API」는 은행·보험·카드·금융투자 등 全 금융권, 나아가 일정한 정부·공공기관, 이동통신사 등을 아우르는 Open API로서,

ㅇ 고객정보를 보유한 ‘금융회사’ 중심에서, ‘정보주체·소비자’ 중심으로 금융산업과 데이터산업을 바꾸어 나가는 기반이 될 뿐만 아니라,

ㅇ API의 개방 외에 해당 기술의 ‘표준화’를 통하여 이에 참여하는 모든 기업이 안전하고 신뢰할 수 있는 방식으로 고객의 데이터를 전송·제공하는 기술적 환경을 마련하게 될 것임

■ 4.30일 Kick-off 회의 이후로 ‘표준 API 최종안’ 마련시까지 약 4개월 간 운영하면서, 분과별 회의, WG 홈페이지 운영 등을 통해 정부와 민간 간, 다양한 금융업권 등 간의 소통 창구로서 역할을 하도록 할 계획

이상과 같이 ISO 20022을 길게 소개한 이유는 금융산업의 폐쇄성을 극복하기 위한 방법으로 표준과 호환성이 중요하다고 생각하기 때문입니다. 그동안 금융결제원, 한국은행, 은행 연구소 및 일본은행 등이 발표한 보고서입니다.

[지급결제조사자료 2018-2] 금융통신메시지 국제표준 ISO 20022 주요 내용 및 시사점

[gview file="http://smallake.kr/wp-content/uploads/2019/05/금융통신메시지-국제표준-ISO-20022-주요-내용-및-시사점.pdf"]

ISO20022 국내 도입 관련 분석 및 시사점

[gview file="http://smallake.kr/wp-content/uploads/2019/05/ISO20022-국내-도입-관련-분석-및-시사점.pdf"]

金融サービスを巡る国際標準化の動向 -ISO 20022の利用拡大とFinTech関連の取組み-

[gview file="http://www.smallake.kr/wp-content/uploads/2018/02/rev17j12.pdf"]

Posted from my blog with SteemPress : http://smallake.kr/?p=26491